Robo Advisors: Crunching the Numbers

Robo Advisors: Crunching the Numbers

Assets under management, avg account sizes and more

Welcome to the post #3 - this one will be about the robo advisors. There’re a lot of speculations on what advisors are performing better, Titan Invest, one of those robo advisors has shared this image in their newsletter:

The question of performance has always been interesting to me, because most robo advisors usually allocate funds into ETFs. Plenty of ETFs are available in the market right now so finding the right allocation might get very complicated at times, but I would assume that all robo advisors trade roughly the same ETFs or have a significant overlap between each other.

I have analyzed the ADV forms - forms that advisors use to disclose their details about clients and AUM - of 14 different firms including robo advisors, classic advisors and one, what can be called a hybrid advisor that provides both auto managed service and has personal financial advisors as well (Vanguard).

New Generation Of Robo Advisors

The first wave of new robo advisors started back in 2007-2008 when such companies as Betterment, Wealthfront, SigFig, Personal Capital and others came to the market. This was the first attempt to democratize the financial advisory market and give access to the advisory services for the larger audience.

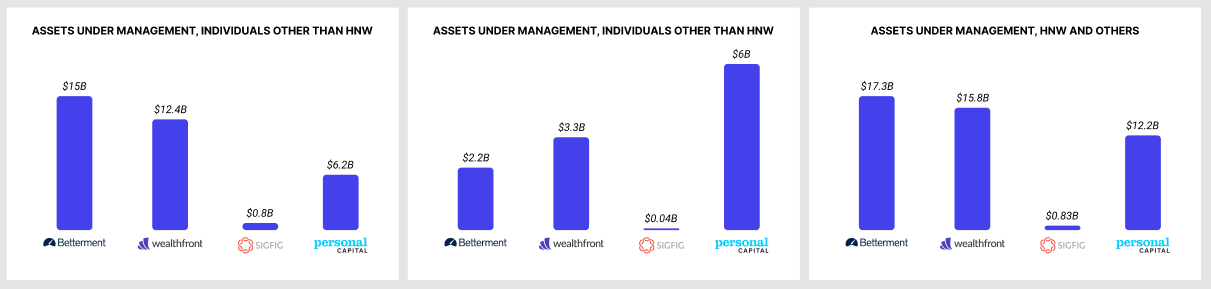

In the reports, advisors break down their accounts into several categories when the most interesting ones are individuals other than high net worth and high net worth individuals. Personal Capital has by far the highest average account size in the section for individuals other than high net worth, when the average account size for high net worth individuals is varying from $1M to $2M for key players:

Betterment is leading in terms of number of accounts. As we can see, SigFig has roughly in the market average account size, but the number of accounts is significantly lower:

Personal opinion - I think SigFig has such a small number of accounts, because SigFig is very tied up to the infrastructure of TD Ameritrade. Based on my personal experience, you have to do a lot of things in the TD Ameritrade client’s portal and only a small part of information is available in the SigFig’s dashboard. This may have changed over time, I had an account with SigFig a few years ago.

Betterment is also leading with the highest total AUM for individual accounts:

Robo Advisors For New Generation

The second wave - new robo advisors launched around 2013-2015. These robo advisors lowered the entry barrier to almost 0 and opened the opportunity for a lot of people to get financial advising services. Acorns and Stash came to the market roughly at the same time - low entry limits, low fees, investing the spare cash - this is what their core message is to get millions of clients. Later both Acorns and Stash started adding more financial services to their platforms.

Stash and Acorns by essentially eliminating the entry barriers targeted a large market. When they started operating back in 2012 (Acorns) and 2015 (Stash), around 50% of the U.S. population could not cover a $400 emergency expense using cash or its equivalent:

The situation has changed and so did Acorns and Stash - now they offer banking products, more sophisticated tools around investing and more. Perfect example of a product growing with its audience and great product-market-fit.

“Classic” Financial Advisors

It’s almost impossible to aggregate all the information for classic investment advisors due to the international nature of their business and a variety of different entities they use to manage their client’s funds.

I checked 4 popular investment advisors - Morgan Stanley Private Wealth Management, BlackRock, Citigroup and J.P. Morgan Securities. Based on the ADV data, Morgan Stanley is an absolute leader by the number of individual accounts other than high net worth with average account size of $318K - roughly the same as Personal Capital’s one:

Classic financial advisors are much more popular among high net worth individuals and as you can see from the chart above, the average account size at Morgan Stanley significantly exceeds the same metric of any robo advisor.

No doubts that those advisors also have higher assets under management - to demonstrate that, you can see the diagram below where large circle is the Morgan Stanley’s alone AUM compared to 9 largest (or most popular) robo advisors, including those that I provided the numbers for in the beginning:

Hybrid Financial Advisor

I’ve never seen anyone mentioning “hybrid” financial advisors, but for the lack of a better word, I think Vanguard is exactly this. Besides the ETF business, Vanguard gives its clients an opportunity to invest in its ETFs with managed accounts and in fact combines the classic financial advisory services when you have some personal help from a professional financial advisor and a self-serve managed account.

Therefore I want to compare Vanguard to the classic financial advisors on average accounts size of high net worth individuals and to robo advisors on average account size of other accounts:

As we can see, Vanguard has a smaller account size for all individuals other than HNW compared to Personal Capital, but has a significantly higher number than other robo advisors. Also Vanguard is in the game with classic robo advisors with average account size above J.P. Morgan Securities and Citigroup, but less than BlackRock and Morgan Stanley.

Worth Mentioning

One robo advisor that is absolutely worth mentioning is Ellevest - the company is building the platform to help women invest. One metric where Ellevest outplays all the robo advisors is the average account size for high net worth individuals. Although the number of such accounts is relatively low and stands at 87, but the average account size is almost at $3M:

The average account size of other than high net worth individuals is around $7.3K which is between what Acorns and Stash have and the first gen of robo advisors - Betterment, Personal Capital, Wealthfront and SigFig.

Key Takeaways

The progress of robo advisors over the past 10-15 years is outstanding, getting to over $50B AUM from an absolute zero is mind blowing. However, it’s still a small portion of what the big wealth management firms are sitting on;

I think that these giants will slowly but steadily adapt to digital reality and will provide more tools and platforms for the larger audience. It does not necessarily mean that they will go after the market of small accounts, but rather reduce their costs of manually managing the funds of their clients. In fact, this industry of wealth management automation has been attracting attention for quite some time now;

Personal Capital is one of the robo advisors that is coming to the edge of a robo advisor and a classic wealth manager in terms of average account size, in fact Personal Capital is capturing the market that will potentially grow significantly in the future - people are becoming more tech-savvy, looking for digital platforms to manage their wealth and Personal Capital is right there;

Personal Capital is another great example of a company that grows with its customers - I remember when I checked the numbers a few years back, Personal Capital had ~$30K average account size, while now it’s 10x higher;

Thanks for reading this post about robo advisors. As usually - feel free to reach out to me on twitter (https://twitter.com/Max_Grigoryev) and share this post with your friends: